All Categories

Featured

Table of Contents

For most people, the biggest problem with the limitless financial concept is that initial hit to early liquidity triggered by the prices. Although this disadvantage of infinite banking can be minimized substantially with appropriate plan layout, the initial years will constantly be the worst years with any kind of Whole Life policy.

That claimed, there are certain unlimited banking life insurance policy policies developed mostly for high very early cash value (HECV) of over 90% in the first year. Nonetheless, the long-lasting performance will usually substantially delay the best-performing Infinite Financial life insurance policy plans. Having accessibility to that additional four numbers in the first couple of years might come at the cost of 6-figures down the roadway.

You actually get some considerable long-term benefits that help you redeem these early expenses and then some. We discover that this impeded early liquidity issue with boundless banking is more psychological than anything else as soon as extensively explored. Actually, if they definitely required every cent of the cash missing from their boundless banking life insurance coverage plan in the initial couple of years.

Tag: infinite financial concept In this episode, I speak concerning finances with Mary Jo Irmen who educates the Infinite Financial Concept. With the surge of TikTok as an information-sharing platform, economic suggestions and techniques have actually found a novel way of dispersing. One such approach that has actually been making the rounds is the unlimited financial idea, or IBC for short, garnering endorsements from celebs like rapper Waka Flocka Fire.

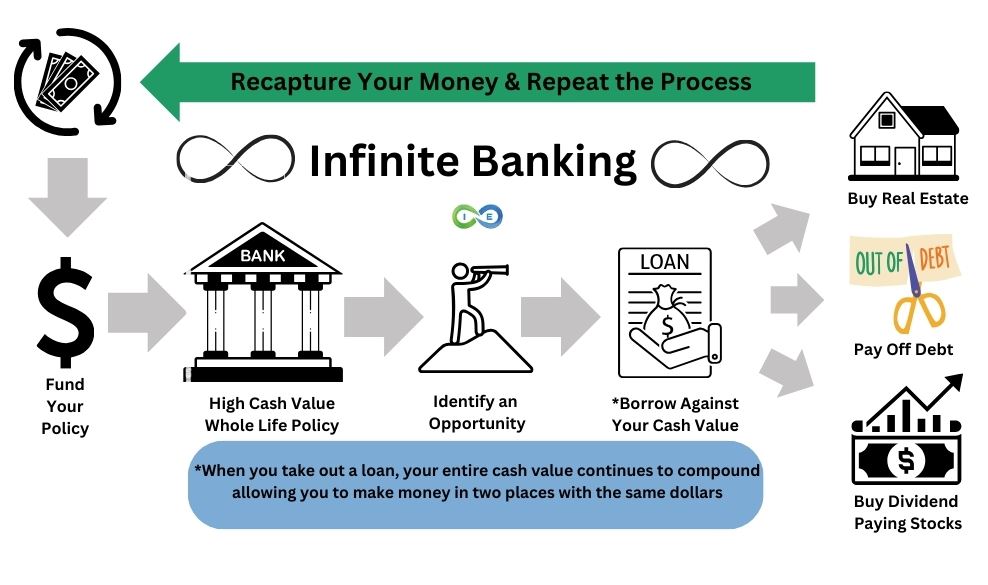

Within these plans, the money worth expands based upon a price established by the insurer. Once a substantial cash money value accumulates, insurance holders can obtain a money value finance. These financings differ from standard ones, with life insurance serving as collateral, indicating one might shed their insurance coverage if borrowing exceedingly without sufficient money worth to sustain the insurance policy prices.

And while the allure of these policies is noticeable, there are innate limitations and risks, necessitating attentive cash value surveillance. The strategy's legitimacy isn't black and white. For high-net-worth people or company owner, particularly those using approaches like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and compound growth might be appealing.

Infinite Banking Concept Youtube

The attraction of infinite banking doesn't negate its challenges: Expense: The fundamental demand, a long-term life insurance policy, is costlier than its term equivalents. Qualification: Not every person qualifies for whole life insurance because of rigorous underwriting procedures that can leave out those with specific wellness or way of living conditions. Intricacy and threat: The detailed nature of IBC, paired with its threats, may deter numerous, particularly when easier and much less high-risk options are readily available.

Alloting around 10% of your month-to-month earnings to the plan is just not viable for many people. Making use of life insurance as a financial investment and liquidity resource requires discipline and monitoring of plan money value. Consult an economic expert to establish if infinite banking lines up with your concerns. Component of what you read below is just a reiteration of what has actually currently been claimed above.

Before you obtain on your own right into a circumstance you're not prepared for, know the following first: Although the idea is generally marketed as such, you're not really taking a car loan from yourself. If that were the situation, you wouldn't have to repay it. Rather, you're obtaining from the insurance provider and need to settle it with passion.

Some social networks posts recommend using cash value from entire life insurance policy to pay down bank card financial debt. The concept is that when you repay the funding with interest, the amount will certainly be returned to your financial investments. However, that's not how it functions. When you pay back the lending, a portion of that interest goes to the insurer.

For the very first numerous years, you'll be paying off the commission. This makes it exceptionally challenging for your plan to collect worth throughout this time. Unless you can pay for to pay a few to several hundred bucks for the following years or more, IBC won't function for you.

Infinite Banking Solution

Not every person ought to depend entirely on themselves for monetary safety. If you call for life insurance policy, here are some beneficial suggestions to consider: Think about term life insurance coverage. These policies offer insurance coverage throughout years with considerable financial commitments, like mortgages, pupil fundings, or when taking care of children. See to it to shop around for the ideal rate.

Copyright (c) 2023, Intercom, Inc. () with Reserved Font Name "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Call "Montserrat".

Bank Cipher Infinite

As a certified public accountant focusing on actual estate investing, I've cleaned shoulders with the "Infinite Financial Idea" (IBC) a lot more times than I can count. I have actually even spoken with professionals on the topic. The major draw, apart from the obvious life insurance policy benefits, was constantly the concept of building up money value within a long-term life insurance policy plan and borrowing against it.

Certain, that makes sense. Honestly, I always assumed that cash would certainly be better spent straight on investments rather than channeling it through a life insurance plan Till I found exactly how IBC might be incorporated with an Irrevocable Life Insurance Coverage Trust Fund (ILIT) to develop generational wide range. Allow's begin with the fundamentals.

Ibc Finance

When you borrow versus your policy's cash money value, there's no set payment schedule, giving you the liberty to handle the car loan on your terms. The cash money value continues to expand based on the plan's assurances and returns. This arrangement enables you to access liquidity without interfering with the long-lasting development of your policy, gave that the lending and passion are managed sensibly.

The process continues with future generations. As grandchildren are born and expand up, the ILIT can purchase life insurance policies on their lives. The count on then collects multiple plans, each with expanding money worths and fatality advantages. With these plans in location, the ILIT effectively ends up being a "Family Bank." Family participants can take financings from the ILIT, making use of the cash money value of the plans to fund investments, begin companies, or cover major costs.

A vital element of handling this Family members Bank is making use of the HEMS criterion, which represents "Health, Education, Upkeep, or Assistance." This standard is frequently included in trust contracts to route the trustee on how they can distribute funds to recipients. By adhering to the HEMS requirement, the trust makes certain that circulations are produced necessary requirements and long-lasting support, safeguarding the trust's possessions while still providing for member of the family.

Raised Versatility: Unlike rigid financial institution finances, you regulate the payment terms when obtaining from your very own policy. This permits you to framework settlements in a manner that lines up with your company cash money circulation. infinite banking nelson nash. Improved Cash Money Circulation: By financing overhead with policy loans, you can possibly maximize cash money that would or else be bound in standard financing payments or tools leases

He has the very same equipment, but has additionally constructed extra cash money worth in his policy and obtained tax benefits. And also, he currently has $50,000 offered in his policy to use for future chances or expenses. Despite its prospective advantages, some people continue to be unconvinced of the Infinite Financial Idea. Let's deal with a few typical problems: "Isn't this simply costly life insurance?" While it holds true that the costs for a correctly structured entire life policy might be higher than term insurance, it's crucial to see it as even more than simply life insurance policy.

Infinite Concept

It has to do with developing an adaptable funding system that provides you control and supplies numerous benefits. When used strategically, it can complement other investments and service approaches. If you're fascinated by the possibility of the Infinite Financial Concept for your service, here are some actions to take into consideration: Educate Yourself: Dive deeper right into the principle with respectable books, seminars, or assessments with educated specialists.

{kind=link}

Latest Posts

Benefits Of Infinite Banking

How Does Infinite Banking Work

How Can I Be My Own Bank